Management of Working Capital Bcom Notes

Management of Working Capital Bcom Notes:-

In this post, you will get the notes of B.com 3rd year Financial Management, by reading this post you can score well in the exam, hope that this post has helped you with this post to all your friends and all groups right now I must share it so that every student can read this post and it can also be helped in this post. Management of Working Capital

Management of Working Capital

CONCEPT OF WORKING CAPITAL

The main concepts of working capital are as follows:

- Quantitative Concept: This is also known as ‘Gross Working Capital Concept’. The main followers of this concepts are Meed, Mallot, Field, Baker, Bonneville and Mill etc. According to this concept working capital is the total of all the current assets. This view places more emphasis on the quantitative aspect of working capital rather than its qualitative aspect. (Management of Working Capital)

According to Meed, Mallot & Field, “Working Capital means Current Assets.”

- Qualitative Concept: This concept is mainly followed by Lincon, Sayors and Stavens. According to this concept the excess of the current assets over current liabilities is known as working capital.

The Need or Objects of Working Capital

- For the purchase of raw materials, components and spares.

- To pay wages and salaries.

- To incur day-to-day expenses and overhead costs such as fuel. power and office expenses, etc.

- To meet the selling costs as packing, advertising etc.

- To provide credit facilities to the customers.

- To maintain the inventories of raw material, work-in-progress, stores and spares and finished stock.

COMPONENTS OF WORKING CAPITAL

There are two components of working capital, viz., Current Assets and Current Liabilities.

- Current Assets: Current assets are those assets which can be converted into cash in the normal course of business within a short period-say a maximum of one year. They are also called floating or circulating assets because they can not be put to constant use. They are meant for resale or produced for the purpose of sale i.e., converting them into cash. In brief, the list of current assets comprises of: (Management of Working Capital)

- Cash in hand and bank balances, 2. Bills Receivables, 3. Sundry Debtors (less provision for bad debts), 4. Short-term loans and advances, 5. Inventories of stocks, as: (a) Raw material, (b) Work-in-process, (c) Stores and spares, (d) Finished goods, 6. Temporary Investments of surplus funds, 7. Prepaid Expenses. 8. Accrued Incomes.

- Current Liabilities: Current liabilities are those liabilities which are intended to be paid in the ordinary course of business within a short period of normally one accounting year out of the current assets or the income of the business. Examples of current liabilities are: Bills Payable, Sundry Creditors or Accounts Payable, 3. Accrued or Outstanding Expenses, 4. Short-term loans, advances and deposits, 5. Dividends Payable, 6. Bank Overdraft, 7. Provision for taxation.

Illustration 1: (i) If cash ₹ 50,000, Debtors ₹ 2,50,000, Creditors ₹ 25,000, Dividend Payable ₹ 75,000, then find out the Working Capital.

(Meerut, 2014)

Working Capital = Current Assets – Current Liabilities

= (Cash + Debtors) – (Creditors + Dividend Payable)

= (50,000 + 2,50,000) – (25,000+ 75,000) = ₹ 2,00,000

(ii) If closing Stock ₹ 50,000, Cash ₹ 2,50,000, Bills Payable ₹ 1,00,000, creditors 1,00,000, then find out the working capital.

Management of Working Capital

(Meerut, 2014)

Working Capital = Current Assets – Current Liabilities

= (Closing Stock + Cash) – (B/P + Creditors)

= (50,000+ 2,50,000) (1,00,000 + 1,00,000) = 1,00,000

(iii) If Current Assets are ₹ 50,000 and Current Liabilities are ₹ 20,000, then find out the working capital.

(Meerut, 2014)

Working Capital = Current Assets Current Liabilities

= 50,000 – 20,000 = ₹ 30,000

(iv) Total Assets ₹ 6,00,000, Total Fixed Assets = ₹ 3,50,00 Reserve and Surplus ₹ 3,50,000. Find out the Gross Working Capital,

(Meerut, 2014)

Gross Working Capital = Amount of Total Current Assets

= Total Assets – Total Fixed Assets

6,00,000 – 3,50,000 = ₹ 2,50,000

KINDS OR CLASSIFICATION OF WORKING CAPITAL

(A) On the Basis of Concept:

(i) Gross Working Capital – Sum of total current assets is called gross working capital,

(ii) Net Working – Capital Excess of current assets over current liabilities is called N Working Capital.(Management of Working Capital)

(B) On the Basis of Need:

(i) Fixed or Regular Working Capital –That amount of working capital which must always be kept the business so that day to day operations of the business could continue without any obstacles, is called fixed or regular working capital. The arrangement of fixed working capital should be made from long-tem sources only, for example share capital, debentures, long-term loans etc.

(ii) Variable/Temporary or Seasonal Working Capital: In certain months of the year, the level of business activities is higher than norm and, therefore, additional working capital may be required along with the permanent working capital. It is known as variable or temporary working capital. Need for temporary working capital should be met from short- term sources of finance, e.g., short-term loans etc. so that it can b refunded when it is not required.

Management of Working Capital

SOURCES OF WORKING CAPITAL

(I) Long-term Sources: (A) Owned Sources: (i) Issue of Shares (ii) Retained earnings, (iii) Reserves, (iv) Sales of obsolete fixed assets (v) Retiring current liabilities below book-value. (B) Borrowed/Extern Sources: (i) Debentures and (ii) Long-term loans/debts.

(II) Short-term Sources: (A) Internal Sources: (i) Depreciation Fund, (ii) outstanding liabilities and (iii) Provision for taxes, (B External Sources: (i) Trade Credit, (ii) Bank Credit, (iii) Short-ter loans from financial institutions, (iv) Public Deposits and (v) Advance from customers.(Management of Working Capital)

Factors affecting Working Capital Or Determinants of Working Capital: (1) Nature and Size of Business, (2) Length of Production Cycle, (3) Seasonal Operations, (4) Business Cycle Fluctuations, Credit Policy relating to Sales, (6) Credit Policy relating to purchase. Availability of Raw Material, (8) Availability of Credit from Banks / Banking Relations, (9) Price level changes, (10) Turnover of Inventories, (11) Dividend Policy. (12) Magnitude of Profit and (13) Operational Efficiency.

Management of Working Capital

Advantages of Adequate Working Capital: (1) Solvency of the Business, (2) Advantage of Cash Discounts, (3) Availability of Raw Materials on Regular Basis, (4) Increase in Debt Capacity and Goodwill, (5) Facilitates the Distribution of Dividends, (6) Exploitation of Favourable Market Opportunities, (7) Regular payment of Wages and other daily expenditures, (8) Full utilisation of Fixed Assets.

Disadvantages of Excessive Working Capital: (1) Unnecessary accumulation of large inventory, (2) Higher amount tied up in debtors and higher incidence of bad debts, (3) Adverse effect on Profitability, (4) Inefficiency of Management.

Management of Working Capital

METHODS OF ESTIMATING WORKING CAPITAL

The main methods of estimation of working capital are as follows:

- Cash Forecasting Method: In this method an estimate is made of the possible cash receipts and payments in the forthcoming period. The estimated cash receipts are added in the working capital available at the beginning of the period and the estimated cash payments are deducted. This shows the deficiency or surplus of cash at a definite point of time. In short, this method is based on Cash Budget.

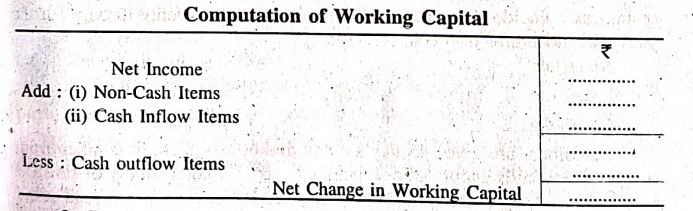

- Adjusting Profit and Loss Method: Under this method the forecasted-profits are adjusted on cash basis. The estimation of working capital requirement by this method can be easily understood by the following format:

Computation of Working Capital

- Projected Balance Sheet Method: Under this method of forecasting, a forecast is made of the various assets and liabilities of the firm. Afterwards, the difference between the two is taken which will indicate either cash surplus or cash deficiency.

- Forecasting of Current Assets and Current Liabilities Method: This is the most popular method of estimating the working capital requirement. It has already been stated that the working capital is the difference between current assets and current liabilities. (Management of Working Capital)In order to estimate the requirements of working capital one has to forecast the amount of current assets and current liabilities. Generally we make the estimate on the basis of past experience related to production process, credit policy and stock policy. In brief, the following points are taken into consideration at the time of estimating the amount of current assets and current liabilities:

(i) The total number of units to be manufactured throughout the year:

(ii) The cost of raw materials, wages and overheads for each unit;

(iii) Information about the period during which raw materials will remain in stock on an average before the same are issued to production;

(iv) Information about the period during which the product will be processed in the factory i.e., the length of the production process;

(v) Information about the period during which finished products will remain in the warehouse before sale i.e., the length of sales cycle;

(vi) Information about the period of credit allowed to debtors;

(vii) Information about the period of credit allowed by suppliers:

(viii) Information about the lag in payment of wages and overheads.”

Management of Working Capital

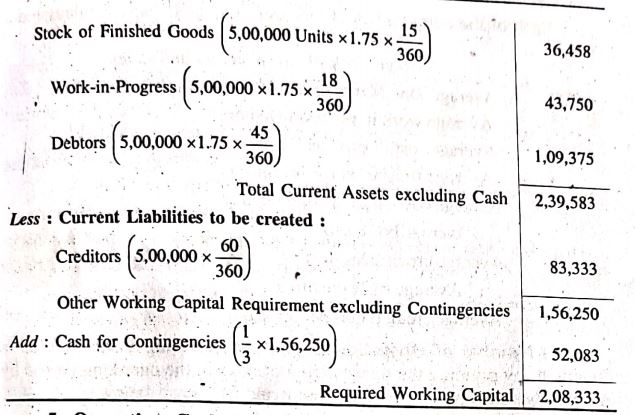

Illustration 2. From the following information, prepare a statement showing the average amount of working capital required by Solvent Ltd. taking 360 days in a year:

Annual sales are estimated at 5,00,000 units at 2 per unit. Production quantities coincide with sales and will be carried on evenly throughout the year and the production cost is :

Customers are given 45 day’s credit and 60 day’s credit is taken from suppliers. 36 day’s supply of raw materials and 15 day’s supply of finished goods are kept. Production cycle is 18 days and all materials is issued at the commencement of each production cycle. A cash balance equivalent to one-third of the average of other working capital requirement is kept for contingencies.

Solution.

- Operation Cycle Method: According to this approach,the requirement of working capital depends upon the operating cycle of the business. The operating cycle begins with the acquisition of raw materials and ends with the collection of receivables. It may broadly be classified into the following four stages. viz., (i) Raw material and stores storage stage;

(ii) Work-in-process stage;

(iii) Finished goods inventory stage; and

(iv) Receivables collection stage.

Management of Working Capital

In this method, the following four steps are involved to estimate the requirements of working capital:

(i) Duration of Operating Cycle: The duration is computed in days by adding together the average storage period of raw materials, works-in-progress, finished goods and the average collection period and then deducting from the total, the average payment period.

Symbolically, the duration of the working capital cycle can be put as follows:

O = (R + W + F + D) – C

Where:

O = Duration of Operating Cycle

Management of Working Capital

R = Raw material average storage period

W = Average period of work-in-process

F = Finished goods average storage period

D = Debtors collection period

C = Creditors payment period.

Each of the components of the operating cycle can be calculated as follows:

R = [Average stock of raw materials and stores / Average Raw Materials and stores consumption per day]

W = [Average work in process inventory / Average cost of production per day]

F = [Average finished stock inventory / Average cost of goods sold per day]

D = [Average book debts / Average credit sales per day]

C = [Average trade creditors / Average credit purchases per day]

(ii) Number of Operating Cycles in Operating Period: This is found out by dividing the total number of days in the operating period by the number of days in the operating cycle as shown below:

Management of Working Capital

N = [P / O]

Where: N = Number of Operating Cycles in the operating period

P = Number of days in the operating period

O = Duration of operating cycle (in days)

Suppose the operating period is one year (360 days) and the duration of operating cycle is 60 days then number of operating cycles in the operating period will be calculated as follows:

N = [360 / 60] = 6 Cycles

(iii) Total amount of Annual Operating Expenses: These expenses include purchase of raw materials, direct labour costs and the overhead costs-calculated on the basis of average storage period of raw materials and the time-lag involved in the payment of various items of expenses. The aggregate of such separate average amounts will represent the annual operating expenses.

(iv) Estimating the Working Capital Requirement: This is calculated by dividing the total annual operating expenses by the number of operating cycles in the operating period as shown below:

Management of Working Capital

R = [E / N]

where: R = Requirement of Working Capital (Estimated)

E = Annual Operating Expenses

N = Number of operating cycles in the operating period.

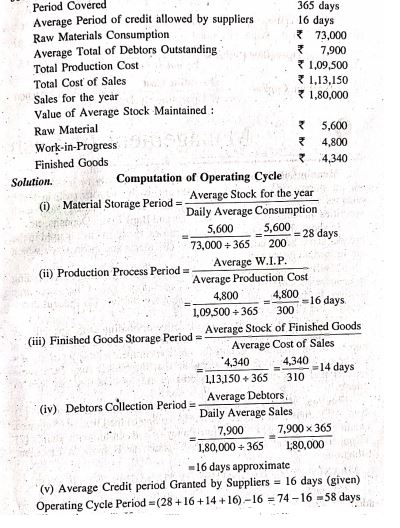

Illustration 3. From the following information extracted from the books of a manufacturing company, compute the operating cycle in days:

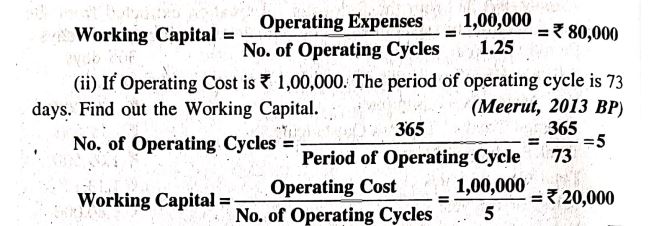

Illustration 4. (i) If operating expenses are 1,00,000 and operating cycle in a year is 1.25, then find out the Working Capital.

(Meerut, 2013 BP)

Management of Working Capital

|

|||