Bcom Cost Accounting Long Question Important Theory Notes

Bcom Cost Accounting Long Question Important Theory Notes :- Hello friends we are posting a bcom cost accounting important question which is very helpful for your exam to making highest marks. in this article we are sharing long question series of fully cost accounting. here you learn easily. and here you can find important links of cost accounting numerical question.

Long Answer Questions

Qus 1. What is Cost Accounting ? Explain its objectives and advantages.

MEANING AND DEFINITION OF COST ACCOUNTING

Ans The system of cost accounting is such a specific branch of general accounting in which accounts of various expenses made over a product or service are prepared in such a way as to obtain informations and data for the guidance of management and to work out the total and per unit cost.

In other words, cost accounting is such a system of accounting in which accounts of expenses are prepared with the objective of knowing and controlling the cost. As a matter of fact, determination, analysis and control of cost is possible only through the informations provided by cost accounting.

Some of the definitions of cost accounting are as follows :

(1) “Costing is the classifying, recording and appropriate allocation of expenditure for the determination of the cost of products or services, and for the presentation of suitably arranged data for the purpose of control and guidance of the management. It includes the ascertainment of the cost of every order, job, contract, process, services or unit as may be appropriated. It deals with the cost of production, selling and distribution.” —Harold J. Wheldon

(2) “Cost accounting is the provision of such analysis and classification of expenditure as will enable the total cost of any particular unit of production to be ascertained with reasonable degree of accuracy and at the same time to disclose exactly how such total cost is constituted.” —Walter W. Bigg

The terms cost accounting, costing and cost accountancy are different from each other but in practice all these terms are used as

Conclusion : The definitions of cost accounting stated above synonyms. depict that cost accounting, which is a specific branch of accounting, is adopted mainly by manufacturing or service rendering undertakings to know the total and per unit cost of a product or service. Cost accounting, in fact, is concerned with the study of cost determination, cost control and profitability. Cost accounting can be properly defined as below : “Cost accounting is classifying, recording and appropriate allocation of expenses for determining the costs of products or services for the control and guidance of management.”

NATURE AND CHARACTERISTICS OF COST ACCOUNTING

The main characteristics of cost accounting can be summarised as follows :

- Cost accounting is a branch of accounting.

- Cost accounting is both art and science.

- Cost accounting is classifying, recording and appropriate allocation of expenditure.

- Total or per unit cost of the product or service can also be known from cost accounting.

- Work-in-progress can also be find out from this system.

- The informations provided by this system can be used in solving several management problems.

- Cost accounts are also helpful in controlling the costs.

OBJECTIVES OR FUNCTIONS OF COST ACCOUNTING

The main objectives of cost accounting are as follows :

- Cost Determination : The main objective of cost accounting is to know the total and per unit cost of products, services, contracts or processes.

- Cost Control : The second objective of cost accounting is to control the cost so that the maximum and better production on minimum cost may be possible. To achieve this objective, the technique of budgetary and standard cost control is adopted.

- Cost Reduction : Cost accounting system controls the expenditure with the objective of cost reduction.

- Guidance to Management : The informations provided by the cost accounts guide the management in policy decisions.

- Determination of Selling Price : One of the objectives of cost accounting is to fix the reasonable sale price so that the competition may be faced and profit may be earned.

- Compliance to Statutory Requirements : Under section 209(1) (d) of the Companies Act, 1956, the central government has made it compulsory for 47 industries to maintain cost accounts. Thus, compliance to statutory obligations is also one of the objectives of cost accounting.

ADVANTAGES AND IMPORTANCE OF COST ACCOUNTING

Cost accounting system has been fully successful in achieving its objectives. Its importance is, therefore, continuously increasing. It is advantageous not only to the manufacturers or producers but to others also. In brief, the advantages of cost accounting may be summarised under the following heads :

I. ADVANTAGES TO PRODUCERS AND MANAGERS

The advantages of maintaining cost accounts to the producers and managers are as follows :

(a) Best utilisation of Material, Labour and Plant : Detailed accounts are prepared in cost accounts for material, labour and plant. Thus, the theft of material and the misutilisation of labour can be easily checked and the best utilisation of the plant can be made.

(b) Knowledge of Profitable and Non-profitable Activities : In cost accounting, separate cost analysis of each job, process, department, product or service is done. It helps in knowing their separate profit or loss. Ifs advantage is that non-profitable activities may be suspended and profitable ones may be continued or efforts may be made to improve the non-profitable activities.

(c) Analytical and Comparative Study of Production Cost : In cost accounting, the cost per unit is calculated by classifying the total cost of production in various costs such as direct and indirect cost, fixed and variable cost, works, office and distribution cost, etc. This analysis reveals the changes in cost and their causes in two periods. It helps in checking the increasing expenses and reducing profits. It also develops the capacity of the organisation to face competition.

(d) Helpful in Fixing Sale and Tender Prices : The cost of production of a product at various stages may be easily known with the help of cost accounts. Thus, the sale price, after adding the reasonable profit in the cost may be easily fixed. The cost accounts are also helpful in quoting the tender price. In cost accounting, the sale price and tender price are fixed keeping in view the cost in the last period and the current trends.

(e) Helpful in Controlling the Cost : Cost accounts provide useful data to the management for planning, budgeting and controlling cost. It helps in controlling the cost with the application of standard costing and budgetary control. Cost comparison also helps in cost control. Thus, cost accounts are helpful in controlling the cost.

(f) Knowledge of Losses or Inefficiencies : Cost accounts not only show the cost of production but also reveals losses or inefficiencies occuring in any form such as idle time, excessive spoilage or scrap, under-utilisation of plant and machinery.

(g) Helpful in Taking Vital Decisions : The informations provided by the cost accounts help the management in taking several important decisions. Whether the management should start manufacturing a new product to supplement their old product or it should be purchased from the market, what should be more profitable product mix and how the unused capacity should be utilised, all such complex problems are solved with the help of information supplied by the cost accounts.

(h) Utility in the Period of Depression : The period of depression is the worst period for producers. During this period, even if the variable cost is fully recovered, the production work may be continued. With the help of cost accounts, the variable cost may

II. ADVANTAGES TO EMPLOYEES

A sound system of costing benefits well performing employees in different ways :

- (i) Employees know in advance the efficiency level expected of them. This imparts clarity to their work methodology and the pace they are required to maintain. Undue work

- (ii) Efficient and inefficient employees get distinguished . This

- (iii) Employees get rewarded in the form of bonus and incentive

- (iv) Employees in general get benefited due to higher growth of the organisation resulting from high level of cost-consciousness. Employees of a profitable and growing organisation enjoy better status, higher security of job and better prospects of career advancement.

III. ADVANTAGES TO CONSUMERS

Cost accounts help in controlling the production cost and in improving the quality of the product because in organisation where cost accounts are maintained, standard raw material and efficient workers are used in production. The advantages of reduction in production cost and improvement in product quality reaches the consumers to a very great extent as they get good quality products at cheaper prices. Thus, cost accounts develop a feeling in consumers that the prices charged from them are reasonable.

IV. ADVANTAGES TO GOVERNMENT

The detailed and analytical informations regarding various industries, provided by the cost accounts, depict their actual position. This helps the government in formulating important policies regarding price determination, price control, wages fixation, dividend payment, fixation of excise duty, exports promotion and import restrictions, etc. It is clear from the above description that maintenance of cost accounting system is not only beneficial to the producers but to every part of the society.

Qus. 2 The ordinary trading account is locked store-house of most valuable information to which cost accounting is the key.” Elucidate te above statement and explain the difference between Financial and cost accounts.

FINANCIAL ACCOUNTING VS. COST ACCOUNTING

Both financial and cost accounts are the branches of accounting. Although their objectives are different yet their methods are one and the same and they are connected with each Other. Both the systems of accounting are usually adopted in various organisations or undertakings. The objective of financial accounting is to show the financial position of the organisation while the objective of cost accounting is to determine and control the cost. These systems of accounting are not competitive but are complementary to each other.

It is clear that though the financial and cost accounts are closely connected to each other yet there are certain similarities and dissimilarities in them.

SIMILARITIES BETWEEN COST AND FINANCIAL ACCOUNTS

As both the systems are the parts of general accounting, similarity in them is quite natural. The main similarities in them

- Both the systems of accounting are based on double entry are as follows :

- Their basic documents such as bills, vouchers, etc. are the

- In both the systems only monetary transactions are taken into account.

- Both the systems show the profit or loss of the business.

- In both the systems, a comparative study of expenditure and profit/loss of various periods is made.

- Both the systems are competent to determine the selling price.

- Both the systems are complementary to each other.

DISIMILARITIES BETWEEN COST AND FINANCIAL ACCOUNTS

The main dissimilarities in these accounting systems are as follows :

- Objective : The objective of financial accounting is to disclose the financial position of the business while the objective of cost accounting is to find out and control the cost of the products manufactured by a business concern.

- Scope : The financial accounts are maintained by all the business, industrial and other organisations while cost accounts are maintained only in those organisations which are either involved ir manufacturing activity or are providing services. Thus, the scope 0 financial accounting is wider than the cost accounting.

- Nature of Accounting Transactions : In financial accounting all the financial or monetary transactions, whether directly concerned with business or not, are recorded while in cost accounting only those transactions, which are related to production or services are recorded. Thus, income tax, interest, dividend, donations, etc. are not recorded in cost accounting because these are not at all related to production or rendering of services. These transactions are, however recorded in financial accounting.

- Necessity of Accounts : For ascertaining tax, every organisation maintains financial accounts while maintenance of cost accounts is essential for certain specific manufacturing companies, as explained in section 209(1) (d) of the Companies Act.

- Audit : Audit of financial accounts is compulsory in the case of all joint stock companies while in case of cost accounts, it is not compulsory in all companies. Sec. 233-B of the Companies Act, 1956, has made cost audit compulsory in certain specified companies to be notified by the Central Government from time to time.

- Figures : Financial accounts deal mainly with actual facts and figures while cost accounts deal partly with facts and figures and partly with estimates.

- Analysis of Profit or Loss : Financial accounts reveals the profit or loss of the entire business while cost accounts show separately the profit or loss of each job, product or process.

- Determination of Sale Price : As financial accounts do not provide scientific basis for determining the sale price, it is illusionary. However, the sale price may be determined more correctly and scientifically on the basis of cost accounts because these accounts provide the detailed information regarding the cost of a product or process.

- Period : Financial accounts are usually prepared for one year* s period. While, cost accounts are prepared monthly, quarterly or for any other period as per requirement of the organisation or undertaking.

- Material Control : financial accounting, only the cost of the material and not the quantity, is shown. Moreover, neither the material cost is classified such ag direct and indiveet nor the efforts are made to control it. In cost accounting, direct indirect materials costs are separately recorded and both the price and the quantity. of material are shown, In addition to it, damages of material are specifically controlled in cost accounting

- Recording of Labour Cost : In cost accounts, separate records are maintaine direct and indirect labour costs and after finding out the efficiency of labour engaged, appropriate incentive plan for increasing their efficiency is adopted. No such action is, however, taken in financial accounting.

- Importance : Financial accounts are the main accounts while the cost accounts are associate accounts. Thus, cost accounts

- Control : In financial accounts main emphasis remains on are of secondary importance.recording of transactions and the importance of control is ignored while in cost accounts sufficient control on expenditure is exercised through cost control, budgetary control and standard costing.

- Presentation : Financial accounts are presented in such a method. way as to fulfill the requirements of company law and income tax law while cost accounts are prepared voluntarily, keeping in view the requirements of management.

The above discussion clarifies that though the financial accounts and cost accounts are closely related to each other yet the financial accounts do not provide such informations to the management of an organisation or business as may be obtained from the cost accounts. For example, from the trading account, prepared under the financial accounts, cost of material during a certain period may be known but it cannot be known as to what is the material cost of each product or process and how much material has lost and where are the possibilities of economy in material used. The trading account gives the consolidated information regarding overhead expenses and gross profit/loss. The financial accounts, therefore, lack in providing separate detailed information regarding each product or process of an organisation. As a matter of fact, detailed information regarding all these aspects is possible only through the cost accounting. Howkins has rightly said :

‘The ordinary trading account is a locked store-house of most valuable information, to which the cost system is the key.”

The above statement emphasises that in the trading account, several valuable informations are hidden but their knowledge is possible only through the use of cost accounting key. The main informations given by the cost accounting system are as follows :

- separate material cost of each product or process.

- normal and abnormal wastages of material.

- loss of material due to obsolescence.

- separate labour cost of each product or process.

- separate income from sale of each product or service.

- separate gross profit from each product.

- percentage of gross profit to sales of each product.

Q. 3. What is meant by cost accounting ? Discuss the characteristics of an ideal system of cost accounting.

Ans. INSTALLATION OF A COSTING SYSTEM

For installing a costing. system in a manufacturing organisation, the following procedure should be adopted :

1. Study of Technical Characteristics : While selecting a method of costing, the technical characteristics of the organisation such as nature of material, capacity of plant, nature and quality of labour, etc., should be properly considered because all these aspects effects the type of costing system to be adopted.

2. Study of Nature of the Product : The nature of the product also affects the selection of a costing system. Thus, the nature of the product should be well studied.

3. Ascertainment of Cost Centres : Cost centre means any such centre where the records of total expenses of a group are maintained. A cost centre is a group of departments, sections, equipments, machines or persons for which data are collected. Cost centres may be of several types such as personal, impersonal, process, etc. For installing a costing system, establishment of cost centres to ascertain the cost at every centre, is essential.

4. Ascertainment of Unit of Cost : The cost centre is related to place, person, equipment, etc. while the unit cost is concerned with the product or service. At one cost centre, several production units may function. Under these circumstances, per unit cost together with total cost at the cost centre, is ascertained. The unit cost may be easy or complex, per dozen, per metre, per ton, etc. are the examples of easy units while per ton km, per passenger km, etc. are the examples of complex units. The selection of cost units depends upon the nature of business.

5. Determination of the Procedure Relating to Cost : In a big business’, cost accounting system should be widely employed while in a small business, its short form should be adopted. It is required, so that the installation expenses of costing system may not be more than its utility in the business.

6. Ascertainment of the Extent of Control : The ascertainment of a costing system also depends upon the extent to which the control on material, labour and overheads is desired.

7. Determination of Forms of Documents : Before selecting a costing system it is necessary to determine the standards and forms of documents to be used in the organisation. The documents and forms to be used may be of different colours so that they may be easily recognised.

8. Determination of Forms of Reports : Important informations are sent to management through cost accounts. The informations are sent in the form of various statements and reports. The reports and statements help in cost control. Thus, it should be decided as to whom and in which form the report shall be sent.

9. Determination of the Status of Cost Accountant : Before installing a costing system, it should be decided as to what shall be the rights and liabilities of the cost accountant i.e. what shall be his status in the organisation. It should also be decided as to whom he shall be responsible and who shall be responsible to him.

CHARACTERISTICS OF AN IDEAL COST ACCOUNTING SYSTEM

An ideal cost accounting system should have the following characteristics :

1. Simplicity : Cost accounting system should be simple and clear so that it may be understood even by a man of general wisdom. Ifits procedure is complex it would be difficult to get the cooperation of employees in its successful implementation. Thus, the system should be quite simple.

2. Elasticity : The system should be quite elastic so that the necessary changes may be possible as are required from time to time in the business.

3. Economy : Economy never gleans lesser expenditure but it really means proper expenditure. The expenditure on the system. should be as much that can be easily bear by the organisation and its advantages comparatively should be more than its expenditure.

4. Adaptability : The necessities of various types of businesses are different from each other. Thus, the system should be as per requirements, nature, conditions, necessities and size of the concerned business. The system should be capable of fulfilling all the necessities so that the product cost may be easily ascertained.

5. Accuracy : The utility of the system depends on its accuracy. Thus, to obtain the desired results, the system should be quite

6. Comparability : The system should be such which can provide necessary information and facts and figures to the management for critical and analytical examinations of the work done. It is possible only when cost accounts provide past data of the concerned business, data of other similar businesses, job or departmental informations, etc. controlling the cost, the characteristic of comparability is essential. Thus, the system should possess the characteristics of comparability.

7. Prompt Reports : The system should be such which can provide the concerned business reports promptly so that the management may take decisions at the right time to control the cost.

8. Classification and Analysis : For the success of the system, it is necessary that the correct and appropriate classification of expenses relating to the production, administration,selling and distribution should be done to lay their reasonable burden on each product, process or job. It helps in determining their total and per unit cost.

9. Reconciliation with Financial Accounts : The system should provide all those informations which may be required to reconcile its results with the financial accounts so that causes of differences in results if any, maybe find out.

10. Support : The system may be accepted as an ideal one only when its implementation is supported by all the departments and persons employed in the organisation.

Q. 4. Explain the different methods of Cost Accounting and state the industries in which they can be applied.

Ans.

DIFFERENT METHODS OF COST ACCOUNTING

Though in all the businesses, the fundamental principles of accounting are one and the same yet the methods of accounting are different in view of nature and characteristics of business. Similarly, the fundamentals of all the cost accounting methods are the same yet keeping in view the industry or business position, a specific method is employed. The main methods of cost accounting are as follows :

1. Unit Costing Method : This method is also known as single or output costing method. This method is employed in those industries where continuous production is carried out and all the manufactured units are identical. This method is adopted in industries such as brick making, flour mills, cloth mills, paper mills, collieries, cement, sugar mills, wine factories, etc. The main objective of this method is to determine per unit cost at each stage of production. In this method, in order to arrive at per unit production cost, the cost statements or cost sheets are prepared and the total expenditure is divided by the total quantity produced.

2. Job or Contract Costing : In businesses where goods are produced on the basis of order or job work, job costing method is adopted. The objective of the system is to ascertain the cost and profit or loss of each job or work. In this method, job cards are separately prepared for each job. This method is adopted by the printers, manufacturers of machinery parts, foundaries and general engineering work shops. When the form of business is large and it continues for a longer period, contract costing method is adopted. For each contract a separate account is maintained. This method is mainly employed in construction works.

3. Process Costing Method : This method is adopted in industries where there is a continuous production and the product of each process becomes the raw material for the next process. In this method, the product is received at the end of each process. Thus, it is necessary to ascertain the total cost and the per unit cost at the end of each process. Separate account, for each process is opened in this method. This method is generally used in industries such as soap making, chemical and medicine manufacturing, paints, foods, etc.

4. Batch Costing : Where for the sake of convenience, the production work is completed in different batches and it is necessary to know the separate cost of each batch, this method is employed. In this method, every batch is treated as a unit of production and to ascertain per unit cost, total expenses of the batch are divided by the number of units produced. This method is mainly used in industries such as bakeries, pharmaceuticals, general engineering, etc.

5. Operating Costing Method : In industries where commodities are not manufactured but the services are provided, this method is employed. This method is adopted by transport undertakings such as bus, railway companies and industries engaged in electricity distribution, hospitals, hotels, etc. In this method cost per unit of service is ascertained.

6. Multiple Costing Method : This method is employed in industries where in the first instance different types of small parts are manufactured and later on by their assembly, final product comes out. For example, it is employed in industries manufacturing typewriters, televisions, motor-cars, radios, sewing machines, machine tools, etc. As various parts differ from each other, a separate method of costing in respect of each component is used. Thus, this method is termed as multiple costing because in it more than one method is employed.

7. Departmental Costing Method : In organisation where productive work is divided into different departments, this method is employed. In this method, separate cost of each department is ascertained.

8. Cost Plus Method : This method is used in industries or undertakings where work is completed earlier and its cost cannot be correctly ascertained in advance. In this method an agreed sum or percentage to cover overheads and profit is added in the actual cost.

9. Target Costing Method : This method is mainly employed in government manufacturing units. In this method, before starting manufacturing work, probable cost is estimated with the help of experienced persons. The cost so estimated is termed estimated or target cost.

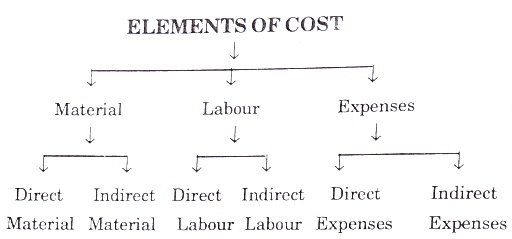

Q. 5. What do you understand by ‘Elements of Cost’ ? Explain different elements of cost.

ELEMENTS OF COST

Ans.

Elements of cost means all those expenses which contribute in the production of goods or services. These expenses may also be said as components or essential parts of cost of a product. As a matter of fact, elements of cost are the primary classifications of cost according to the factors upon which expenditure is incurred. The various elements of cost may be conveniently divided into three parts viz. : (1) Material, (2) Labour and (3) Expenses. Each of these can be direct or indirect.

- Material : In the elements of cost, material has an important place because no goods can be produced without material. Material cost is usually a larger part of the total cost of a product. It can be direct as well as indirect.

- Direct Material : The material which is directly used in Production and which becomes an integral part of the finished goods is termed as direct material. Direct material has physical existence in the goods produced. In simple words, it is the material with which the goods are manufactured. For example sugar is manufactured by sugarcane, furniture by timber, cloth by yarn, etc. Some examples of direct material are given below :

- The material which is used directly in production like sugarcane in sugar industry, timber in chair or table, cloth in shirt.

- Material purchases for specific job or order. For example, bricks and cement are purchased for construction work.

- The product of a process which becomes the raw material for the next process. For example, in a cloth mill, the product of the spinning process becomes the direct material of the weaving process.

- Material which is issued from the store for completing the production work.

- Indirect Material : Material which is used indirectly in production is termed as indirect material. In other words, a material which is neither directly used in production nor becomes the integral part of the finished goods is termed as indirect material. The oil is used to keep the machinery in working order, the cloth is used for cleaning the machinery parts, etc. are the examples Of indirect material. However, in some cases, though material forms a part of finished product yet it is treated as indirect material, e.g., thread used in shirt stitching, nails in shoes. This is because value of such materials is small and it is quite difficult and futile to measure them. According to ICMA, “Indirect material cost means material cost which cannot be allocated but which can be apportioned to or absorbed by cost centres or cost units.”

- Direct Material : The material which is directly used in Production and which becomes an integral part of the finished goods is termed as direct material. Direct material has physical existence in the goods produced. In simple words, it is the material with which the goods are manufactured. For example sugar is manufactured by sugarcane, furniture by timber, cloth by yarn, etc. Some examples of direct material are given below :

- Labour : Labour is another important element of cost. The wages paid to the labour, employed in production, are included in the production cost as labour cost. Like material, labour can be divided into two parts viz., (i) direct labour and (ii) indirect labour.

- Direct Labour : Labour which are directly engaged in production or manufacture of goods is termed as direct labour. In simple words, it is the labour which can be specifically related to particular product, job work or process. For example, labour employed to manufacture furniture or to work on machines is direct labour. Direct labour is also termed as productive labour, factory labour, operating labour, etc. According to ICMA, “Direct wages : Wages which can be allocated to cost centres or cost units.’

- Indirect Labour : Labour which are not directly engaged in production operations but which helps in production operations is indirect labour. Such labour does not alter the condition or composition of the product. Wages paid to foremen, inspectors, time-keeper, store-keeper, gate-keeper, etc. are the examples of indirect labour cost. According to ICMA, “Indirect wages : Wages which cannot be allocated but which can be apportioned or absorbed by cost centres or cost units. “

- Expenses : All expenses other than material and labour which are incurred in production, administration, selling and distribution are termed as expenses. These expenses can also be direct or indirect.

- Direct Expenses : All expenses other than direct material and direct labour which are directly incurred on a specific product, job or process are called as direct expenses. In other words, expenses which can be directly related to the cost of a particular product are termed as direct expenses. Payment of royalty for extracting minerals from mines, excise duty, rent for equipments used in a specific production, fee for drawing designs and charts for a specific job, etc. are the few examples of direct expenses.

- Indirect Expenses : Expenses which cannot related to specific work, job or process but which are related to the whole production, several jobs or processes, are termed as indirect expenses. The benefit of indirect expenses goes to more than one cost centres or units. The remuneration paid to the expert for repairing the machines of all the departments, is an example of indirect expenses. The different elements of cost can be presented in the form of the following chart :

DIFFERENCE BETWEEN DIRECT COST AND INDIRECT COST

Direct costs :- are those costs which are incurred for and may easily and conveniently be identified with a particular cost unit or cost centre (i.e., particular product, particular job, particular contract, particular process). Direct costs include direct material cost, direct labour cost and other direct expenses.

Indirect costs:- on the other hand, represent the costs which are of general nature and which cannot easily and conveniently be identified with a particular cost unit or cost centre. They include indirect material cost, indirect labour cost and other indirect expenses. Indirect costs are also called overheads. They need to be distributed to various cost centres and/or cost units on some reasonable basis. These indirect costs can further be divided into three sub-categories as factory overheads, administration overheads and selling and distribution overheads.

Thus, direct costs of a product or activity can be accurately determined while the indirect costs have to apportioned to various cost units on some arbitrary basis since these costs can not be accurately ascertained.

Q. 6. Explain the different components of total cost with examples.

Ans.

CLASSIFICATION OF COST OR COMPONENTS OF TOTAL COST

A cost statement is prepared to • know the total cost of production. In this statement, the total cost is classified on the basis of elements of cost, as follows :

(1) Prime Cost : Prime cost is also called as direct cost, first cost or flat cost. The main objective of knowing the prime cost is to Divide the total cost into direct and indirect costs. The total of all direct costs is known by the sum of direct material, direct labour and direct expenses and is called as prime cost.

Prime cost = Direct material + Direct wages + Direct expenses

(2) Works Cost or Factory Cost : The objective of knowing the works or factory cost is to control the factory cost and to know the efficiency of the factory. Works cost is also known as production cost or manufacturing cost. If costs of indirect material, indirect labour and indirect expenses of the factory are added to prime cost, works cost is arrived at.

Works cost = Prime cost + Indirect material + Indirect wages + Indirect expenses of the factory

(3) Office Cost : If administrative and office overheads are added to factory or works cost, office cost is arrived at. This cost is also termed as administrative cost or the total cost of production.

Office Cost + Works cost + Office overheads

(4) Total Cost : If selling and distribution overheads are added to office cost, the total cost is arrived at. It is also termed as cost of sales.

Total Cost = Office cost + Selling and distribution expenses

(5) Selling Price : If the desired profit is added to the total cost or cost of sales, the selling price is arrived at. The difference between the selling price and the total cost shall be the profit or loss.

Selling Price = Total Cost + Profit

Profit = Sales — Total Cost

Q. 7. Explain clearly the concept of Material Mention the main requisites of an adequate system of materials control.

Ans. Meaning of Material Control : Material control means taking care of materials and their cost from the stage of procurement to the stage of their ultimate consumption. It includes procuring, storing and supplying of material required for production, at the lowest cost per unit, consistent with the required quality and with the least investment in inventory. Material control function ensures uninterrupted flow of materials to production without carrying unnecessarily large stocks.

Material control may be defined as “systematic control and regulation of purchase, storage and usage of materials in such a way so as to maintain an even flow of production and at the same time avoiding excessive investment in inventories. Efficient material control cuts out losses and wastes of materials that otherwise pass unnoticed.”

OBJECTIVES OF MATERIAL CONTROL

The main objectives of material control are as follows :

- Procurement of materials and stores from suppliers at the lowest price, consistent with the standard specification as to quality and timely delivery;

- Avoidance of production hold-up for want of materials;

- Maintenance of even flow of control;

- Prevention of excessive investment in material stock;

- Avoidance of losses occasioned by deterioration due to evaporation, drayage, careless handling of materials and supplies, pilferage, obsolescence, etc., and

- Making available, accurate and reliable information about the different items of materials and stores for proper planning and control.

ESSENTIAL REQUIREMENTS OF MATERIAL CONTROL SYSTEM

Ideally, a material control must ensure that the following

requirements are fully met :

- There should be proper co-ordination and co-operation between various departments dealing in materials viz, Purchasing Department, Stores Departments, Receiving and Inspecting Department, Accounting Department, etc.

- There should be central purchasing department under the control ofa competent and expert purchase manager.

- There should be proper classification and codification of materials.

- Material requirements should be properly planned.

- The perpetual inventory system should be operated so that up-to-date information is available about the quantity of material in stock.

- Adequate records should be introduced to control materials during production and quantities manufactured for stock.

- The storage of all materials should be well planned subject to adequate safeguards and supervision.

- The various stock levels like minimum, maximum, etc. should be fixed for each item of material.

- Purchase of materials should be controlled through budgets.

- An efficient system of internal audit and internal check should be operated so that all transactions involving materials are checked by reliable and independent persons.

- There should be regular reporting to management regarding purchases, issues and stocks of materials. Special reports should be prepared for obsolete items,spoilage, returns to suppliers, etc.

TECHNIQUES OF MATERIAL CONTROL

The techniques commonly used for material control are as follows :

- Determination of Stock Levels

- Economic Order Quantity

- Material Turnover Ratio

- ABC Analysis

- Perpetual Inventory System

- VEDAna1ysis.

Q. 8. What do you understand by Minimum Stock Level, Maximum Stock Level, Re-order Level and Average Stock Level ?

Ans. Types of Stock Levels : In order to safeguard against under-stocking and over-stocking, the following stock levels are determined :

(1) Minimum Stock Level : The minimum stock level is the lowest quantity of stock which must be maintained in hand at all times so that the manufacturing activity may not stop due to non-availability of materials. The determination of minimum stock level depends upon re-order level, average usage rate, average delivery time, etc. The following formula is used to know this level : Minimum Level Re-order level — (Average usage rate x Average re-order period)

(2) Maximum Stock Level : The maximum stock level is that quantity of material above which the stock should not generally be allowed to go. If the stock, more than the maximum level is Inaintained, it increases the cost of storage, unnecessarily blocks up the capital and increases the possibility of losses on account Of deterioration and obsolescence. Thus, this level is fixed for avoiding over-stocking of the material and its associated risks. The determination of maximum stock level is affected by average usage rate, re-order level, delivery period, possibility of obsolescence, storage facilities, government restrictions, etc. The following formula is used to know this level .

Maximum Level = Re-order level + Re-order quantity — (Minimum usage rate x Minimum lead time)

(3) Re-order Level or Re-order Point : The level of stock of material at which, on reaching the material in store, further order must be sent, is called re-order level or re-order point. This level is fixed somewhere between the maximum and minimum level. This is fixed in such a way that by re-ordering in the normal course of events, new suppplies will be received just before the minimum level is reached. 1 his level can be known from the following formula :

Re-order Level = Maximum usage rate x Maximum lead time

(4) Average Stock Level : The level of stock of material which is generally kept in the store is called average stock level. It is calculated by applying the following formula :

Average Stock Level = Maximum stock level/2 + Minimum stock level/2

The following formula is also used for calculating the average stock level :

Average Stock Level = Minimum stock level + (1/2 of re-order quantity).

Q. 9. Explain the important methods of pricing of materials issued and state which of these methods is best in your opinion ?

Ans. PRICING OF MATERIALS ISSUED

To know the separate cost of each product or job, correct pricing Of materials issued is essential. But it is a difficult task. The materials issued from the store are purchased on different dates and at different prices. Generally the purchase price and the market Price is also differ. At what rate the materials issued from the store should be priced, it is an important question.

The principal methods, of pricing of material issues are as follows :

(A) COST PRICE METHODS

(i) First in First Out Method (FIFO) : Under this method, the materials first received in the store are the first issued i.e., the order in which the materials are received in the store are issued at their cost price in the same order. Thus, the FIFO method follows the principle that materials received first are issued first. After the first lot or batch of material purchased is exhausted, the next lot is taken for supply. The inventory is priced at the latest costs.

This method is most suitable in a period of falling prices because issues are charged at the oldest prices which are higher. This facilitates recovery of higher costs incurred in the past from the product. Closing stocks are valued at latest prices which are lowest.This results in lower value of closing stock; therefore lower book profits and lower tax liability.

Advantages : The following are the advantages of the method :

1. This method is easy to understand and simple to operate.

2. The old material is issued first. Thus, there remains no possibility of loss of material due to spoilage or obsolescence.

3. The price of the material in hand at the end is found almost equal to the market price of such material.

Disadvantages : The main disadvantages of the method are as follows :

1. It is very difficult to separately store the material purchased at different prices and on different dates.

2. The price of the material issued to different jobs on the same date may be different.

3. As the material is issued on old prices, the production cost may not be equal to the market price.

(ii) Last in First Out Method (LIFO) : In this method, the materials purchased in the last are first issued on the cost price. For pricing materials issues,the price of the last purchase is used unless it is fully exhausted. When it is exhausted, the material purchased

This method is suitable in a period of rising prices because material will be issued at the prices of latest purchases which are same as or close to current market price of materials. Closing stock is valued at earliest prices which are the lowest giving lower value of closing stock and therefore lower book profit. As a result the tax liability is also lower. This method thus helps in showing a lower profit because of increased charge to production during periods of

Advantages : The following are the advantages of the system :

1. This method is easy to understand and simple to calculate.

2. As the issue price remains almost equal to the market price, the cost price of the product or job can be easily known.

Disadvantages : The disadvantages of the method are as follows :

1. The closing stock is priced at a very old price which does not show the correct position of the business.

2. The method is not practical because in practice the material which is purchased first, is issued first.

3. More space is needed for separately storing the material purchased at different prices.

(iii) Highest in First Out Method (HIFO) : In this method, the materials purchased at the highest price are first issued irrespective of the date of purchase. After this, the material of the next highest price is issued. This method is based on the principle that the highly priced material should be consumed at the earliest. Thus, in HIFO method, the production absorbs the high cost of materials and closing stock is valued at lower rates. This method is mainly used in case of cost plus contracts or monopoly products as it is helpful in increasing the price of the contract or products.

This method is very suitable in fluctuating market because cost of heavily priced materials is recovered first and inventory valuation is kept at lowest which leads to the creation of a secret reserves. But this method has not been adopted so widely.

(B) AVERAGE COST PRICE METHOD

Under this method, the material is issued at the average cost price irrespective of the date and price of purchase. The following are the forms of this method :

(i) Simple Average Method : Under this method, for determining the issue price, the quantity of material purchased is not considered. The average price is calculated by adding the prices at which materials on different dates were purchased during the Period and dividing the total of these prices by the number of prices taken into consideration for calculating the average price. In other words, simple average price is calculated by dividing the total of prices of materials in the stock from which materials are issued by the number of prices entering in the calculation. This method is SUitabLe when at every time, the material in almost equal quantity is issued and there is no much variation in the purchase price of materials.

Advantages :

1. This method is a mixed form of market price and cost price.

2. Due to calculation of average of different purchases prices, the tendency of equality in different rates is arrived at.

Disadvantages :

1. In case of fluctuations in the quantity of material purchased on different dates, the results become unreliable.

2. It becomes difficult to calculate the average again and again.

(ii) Weighted Average Method : Under this method, for determining the issue price, the quantity of material available in the stock and the price both are considered. •In brief, the weighted average price is calculated by dividing the total cost of available material on the date of issue, by the total quantity of available material. At this price, the material is issued. This method of pricing is suitable for those materials, the prices of which fluctuate more.

Advantages :

1. This method is scientific and argumentative because under this method, the total cost of the material available in the bin is divided by the total quantity of material. In fact, after reaching the bin, the new and old material mix up i.e., there remains no separate existence in the bin, of the material separately purchased on the different dates.

2. As regards to calculation work, this method is simple because the issue price once calculated continues till the new material is purchased.

3. This methodis amixed form ofmarket price and cost price.

4. In this method, the balance of the closing stock is shown at appropriate price which can be used in financial accounts also.

Disadvantages :

I. If the materials is purchased again and again at short intervals, the calculation work increases.

2. As the material is issued at average price, the production cost cannot be correctly estimated.

(C) OTHER METHODS

(i) Replacement Price Method : This method is also known as substitute price method or market price method. Under this Method, the issue of materials is priced at that price on which materials can be purchased on the date of issue. Thus, the cost of materials is totally ignored and the market price of the material on the date of issue is used. This method is appropriate to those businesses where the current price of the materials used in production, are always available.

(ii) Standard Price Method : Under this method, the issue of materials, instead of being priced at actual price, is. priced at a predetermined price which is termed as standard price. The standard price is determined after taking into account all those factors which effect the price of the material. As in the method, the price of material issues always remains fixed, it is also termed as fixed price method. The difference between the actual cost and the standard cost is recorded in the price variance account. This method is appropriate only for those businesses where advance contracts for the purchase of the material in future can be made or where the cost of future purchase of materials can almost be correctly estimated.

(iii) Inflated Price Method : In case the certain materials wastages or loss of weight due to seasonal or other effects is unavoidable, then such wastage or loss of material due to natural and general reasons, is included as a part of the production cost. When after adjusting the loss due to wastage in the purchase price, the material is issued at an inflated price, it is termed as inflated price method. As a matter of fact, this is not a distinct method of pricing but only a procedure for accounting adjustment. It is, therefore, used in conjunction with one of the other methods like FIFO, LIFO, etc.

SELECTION OF AN IDEAL SYSTEM OF PRICING THE MATERIAL ISSUES

Several methods of charging price of material issues have been discussed in detail. The question is as to find which out of these methods is best one. It is a fa@t that no one method can be suitable for all businesses or industries. Thus, keeping in view the conditions of business it should be decided as to which method has to be adopted. Usually, the weighted average method’ is accepted as the best method. However, while selecting an ideal method the following factors should be considered .

1. Type of business or industry.

2. At what intervals, the material is purchased.

3. How much quantity of material is purchased.

4. How much material is generally issued at a time.

5. The market price of the concerned material remains almost, fixed or it fluctuates very much.

6. The role of current prices of material in the cost.

Q. 10. What is• an incentive plan for wage payment ? Discuss its importance. Distinguish between Halsey and Rowan system of wage payment.

Ans. Meaning of Incentive Plan for Wage Payment : Any wage system in which payment is made by results has an element of incentive. The results produced by a worker may be measured in terms of time saved or the excess output turned out by him. In other words, Incentive wage payment methods increase the production by giving an inducement to the workers in the form of higher wages for less time worked. Under incentive plan, a standard time is fixed for the completion of a specific job or operation rand if the job is completed in less than the standard time, workers get a certain fraction of the time saved wages by way of a bonus. Moreover, minimum wages are guaranteed to all workers.

Incentive plans aim at removing defects of time and piece wage systems and attempt to combine the advantages of both. They also attempt at sharing the benefits of efficient performance between workers and the employer because both contribute to efficiency improvement—workers through better effort and employer through providing better machines, tools and other supports. In case workers are paid on time basis, they get no benefit of higher productivity. In case of piece wage entire benefit of higher productivity goes to the worker. In case of incentive plans, the benefit of time saved due to higher than the predetermined output is shared between the worker and the employer resulting in economy in per unit labour cost and overhead cost.

Characteristics of Incentive Plans : The following are common characteristics of incentive plans :

- Workers are guaranteed a minimum wage.

- Efficient workers have a scope of earning an incentive or premium or bonus for time saved.

- Standard time is pre-determined for completing a job or per Time and motion studies are-undertaken for determining

TYPES OF INCENTIVE WAGE RATE SYSTEM

Some of the important incentive plans are as follows :

(i) Halsey Premium Plan

(ii) Rowan Premium Plan

(iii) Taylor Differential Piece Rate Plan

(iv) Merrick Multiple Piece Rate System

(v) Gantt Bonus Plan

(vi) Emerson Efficiency Plan

(vii) Bedaux Plan.

(i) Halsey Premium Plan : F. A. Halsey, an American Engineer, invented this plan in 18 This scheme is known Halsey Premium Plan by his name. In this scheme standard time and standard work are fixed in advance i.e., it is decided what time should be spent in a particular work. If worker is unableü) complete target i.e., standard work, he is provided remuneration on the basis Oftime actually spent by him in performing work. But those workers are able to complete the work before the standard time; they are Provided with extra wages as bonus or premium for the time saved In doing work. The rate of bonus may be 10% to 90% depends upon the particular concern in which the worker is engaged. But if nothing is given in question about percentage of bonus, 50% bonus is provided. In short, the wage is calculated under Halsey scheme as follows :

Wage for the actual time taken Time taken * Rate per hour

Bonus (Premium) = Time saved * Rate per hour * Percentage of bonus

Total wage Wage= for actual time taken + Bonus or Premium

Example : If in order to do any job work, standard time required is 12 hours. Actual hours taken are 10. Wage rate per hour is Rs. 1•5. The wage under Halsey Plan will be as follows :

Advantages of Halsey Plan :

- It is very simple to understand.

- It assures minimum wages to workers.

- The employers also get the advantage of increase in worker’s efficiency.

- Efficient workers are motivated to do more work.

- Provides incentive for efficiency but does not penalise below average workers.

Disadvantages of Halsey Plan : These are as follows :

- Quality of output suffers as the workers are in haste to save time.

- It is a difficult task to determine standard time. Fixation of standard time on the basis of performance of the most efficient worker shall be of no use since all the workers shall finish the work beyond the standard time. Thus, proper time and motion study should be carried out and there should be scientific determination of standard time.

- Careful supervision is necessary to ensure the workers eagerness to work fast, do not waste materials or damage machine and tool carelessly.

- Workers do not like to share the benefits of their efforts in saving time with the employer.

- At higher level of efficiency the earning reduces. Therefore, it does not act as a sufficient incentive.

(ii) Rowan Premium Plan : Mr. James Rowan introduced this scheme in Glasgow in 1898. It is an improvement over Halsey plan. This plan was executed in 1901 by James Rowan. Rowan Plan differs from the Halsey regarding calculation ofbonus. The workers get wages at an hourly rate for the actual time spent on thejob under this plan also. Besides the guaranteed minimum wages, they get a bonus if the task is finished before the predetermined standard time as is in the case ofllalsey Plan. But under this plan bonus is that portion of wages of actual time taken which the time saved bears to the standard time in place of 50% or so as in the case of Halsey plan.

In brief, the wage is computed as follows :

Advantages of Rowan Plan : It has all the advantages of Halsey Plan. Apart from that it has the following advantages :

(I) Quality of output does not suffer to the extent it does in Halsey Plan.

(2) Workers get more premium under this plan than under Halsey plan upto the saving of50% ofstandard time.

(3) Since bonus declines at higher level ofefficiency (i.e., if time saved is more than half of standard time) the worker does not over work and consequently over production can be controlled.

(4) It provides good incentive for comparatively slow workers and learners.

Disadvantages of Rowan Plan :

(1) The employers share the bonus earned by workers. So, the workers remain dissatisfied.

(2) Incentive is not so attractive as it is in case of piece work rate, or Halsey plan on saving of more than 50% time.

(3) It is a complicated system not easily understandable by the workers.

(4) There is an anomaly in the operation of this plan. That is, a worker who saves —th of standard time and a worker who saves ‘thos standard time get the same amount of bonus.

COMPARISON BETWEEN HALSEY PLAN AND ROWAN PLAN

There are lot of similarities and some dissimilarities between Halsey Plan and Rowan Plan. These are as follows :

Similarities :

(i) Both the plans guarantee time wage to the workers.

(ii) Under both the plans the workers do not get the full benefit of time saved by them.

(iii) In both cases cost per unit comes down with increase in efficiency.

Dissimilarities :

(i) Under Halsey Plan bonus is generally set at 50% of the wages of time saved by the worker. Under Rowan Plan bonus is that proportion of the wages of time worked which the time saved bears to the standard time.

(ii) Under Halsey Plan, the effectively hourly wage rate is lower upto 50% of the time saved and can be doubled thereafter. Under Rowan plan it is higher upto 50% of the time saved and falls thereafter. Generally it is difficult to save more than 50% of the standard time. Therefore workers have preference for Rowan Plan

(iii) In the Rowan Plan, the quality of work does not suffer much. The worker is not induced to rush through the work because bonus increases at a decreasing rate at higher levels ofefficiency. In the Halsey Plan, a worker is induced to rush through the work because he gets extra wages for every 50% of the time saved. Hence, Rowan Plan does not induce workers to attempt excessive speeding up as in case of Halsey Plan. Therefore, risk to quality of work is less under Rowan Plan.

(iii) Taylor’ Differential Piece Rate Plan : This plan was originated by F. W. Taylor, who is known as the father of Scientific Management. The main features of this plan are :

- A standard level of work is decided on the basis of time, motion or fatigue study.

- There shall be two piece work rates—one higher rate and another lower rate.

- If the worker finishes work within standard time or works more than standard work in standard time, he will be paid higher piece rate.

- If the worker does not complete standard work in standard time, he will be paid lower piece rate.

In this system the unskilled workers are penalised by paying low rate and efficient workers are encouraged by giving them higher rate.

(iv) Gantt Bonus Plan : This plan is a mixed form of time, piece and bonus systems. In this plan standard time for completing work is decided and time wage as well as higher rate are determined. If a worker finishes the work within standard time, then he will be paid on time basis. But if he finishes work in standard time, he will be paid time wage as well as a bonus at the rate of 20% of time wage. If any worker works more than the standard, he is paid at standard time for actual work plus bonus at the rate of 20%.

Q. 11. What is the difference between apportionment of overheads and absorption of overheads ? What are the different methods of absorption of factory overheads ? Discuss any two of these in detail giving their merits and demerits.

Ans. DIFFERENCE BETWEEN APPORTIONMENT AND ABSORPTION OF OVERHEADS

The allotment of proportions of items of cost to cost centres is called apportionment of overhead while the allotment of overhead to cost units is called absorption of overhead.

The following are the points of difference between the two :

(i) Under the apportionment, allotment of proportion of items of cost to cost centres is done. In this way, under apportionment of overhead, the specific portion of overhead of any department is determined while under absorption, the allotment of overhead to cost unit is done.

(f) The process of absorption starts after the completion of process of apportionment i.e., without apportionment absorption cannot be made.

(iii) Proper proportion/ratios are used under apportionment while under absorption of overheads, the percentage rates of overheads are used.

ABSORPTION OF FACTORY OVERHEADS

Absorption of factory overheads refers to charging of the factory overheads of a particular production department to various products manufactured, or jobs completed, or orders executed in that department. The methods for absorption of these overheads may be put into the following categories :

(1) PERCENTAGE ON DIRECT MATERIAL COST METHOD :- In this •method, the cost of direct materials used in the manufacture of a product is used as the base for allocation of factory overheads. Thus, overhead rate is computed on the basis of the following formula :

Factory Overhead Rate = Amount of Factory Overheads / Cost of Direct Material used * 100

Example : Direct material used amounting Rs. 40,000 in a production department and the factory overhead is Rs. 10,000, then percentage of factory overhead over cost of direct material used 10,000 (Absorption Rate) will be

10,000/4,000 * 100 = 25 % If Rs. 4,000 have been 40,000 spent on material for this department to complete a sub-work, the factory overhead to complete this sub-work Will be 4000*25/100 = Rs. 1000.

Suitability : This method is suitable only where :

(i) Material cost forms the major part of the total cost.

(ii) Overheads tend to relate to material cost.

(iii) Where output is uniform i.e., where only one kind of article is produced and, -therefore, the material charged to each cost unit is the same.

Limitations :

(1) Price of materials are subject to frequent change. so, overheads also change frequently.

(2) Where many machines are used in a factory; overheads are more related to machine hours and not to the cost of materials.

(3) Overheads are more related to the time consumed in the performance of a job. If an efficient worker takes less time and an ineffcien•t workers takes a long time, it is immaterial in this method.

(4) Ifornaments ofgold costing Rs. 10,000 of material are made and on the other hand, ornaments of the same size and weight are also made of copper costing Rs. 100 of material, then the factory expenses incurred in both the cases will not be much different from each other. But if the overheads are absorbed on material basis, it will make a significant difference. So this method is not appropriate in such cases.

(2) PERCENTAGE ON DIRECT WAGE METHOD

Under this method, an actual or predetermined rate of overhead absorption is calculated by dividing the factory overhead to be apportioned or absorbed by the wages paid or expected to be paid. The formula for computincy the percentage rate for a period is given below :

Percentage of Factory Overhead = Factory overhead / direct wages *100

After getting aforesaid percentage, on the basis of that, the factory overhead is charged to the direct labour used in completing any product or sub-work. Example : In the production department of a factory, the factory overhead and cost of direct labour are Rs. 2,500 and Rs. 50,000 respectively. The percentage of factory overhead over direct Rs. 2,500 / 50000 * 100 = 5%. Therefore, the factory overhead wage will be will be absorbed @ 5% of direct wage to different sub-works of production department. If the direct labour cost is Rs. 1,200 then the amount charged for fictory overhead will be Rs. 1200*5/100= 60 rupee.

Suitability : This method is suitable in following cases :

(i) When wages form the greater part of the total cost.

(ii) There is no variation in the wage rates of the different categories of the workers, i.e., the wage paid give a fair indication of the time required to complete a particular job.

(iii) There is uniform efficiency and productivity, i.e., the workers in the department are more or less of the same efficiency.

Advantages : This method has the following advantages :

(i) It is a very simple method and can be applied very easily.

(ii) This method has given recognition to time factor to some extent.

(iii) Total overheads recovered will not differ much from the estimated figure because the total Wages paid will not fluctuate much.

Disadvantages :

(i) This method is not suitable where both skilled and unskilled workers are employed. As a matter of fact, the amount of works overheads is less for skilled workers in comparison to the unskilled workers and, therefore, jobs done by the unskilled workers should be charged with greater amount of factory overheads, but reverse happens in the case of this method.

(ii) Works overheads also depend upon time. This method, therefore, does not give satisfactory results where the workers are remunerated on piece wage system.

(iii) No distinction is made between manual work and machine work. The work done by machinery involves heavy factory overheads in the form of depreciation, etc. which are not necessary where work is done by hand.

(3) PRIME COST METHOD

Prime cost is the aggregate of direct material and direct labour. If the overheads of a department are divided by the prime cost of that department, we get the overhead rate. It is a very simple method. The formula for calculating the factory overhead rate, therefore, can be put as follows :

Factory Overhead Rate = Factory overhead / prime cost * 100

Prime cost

Example : The Material Value is Rs. 10,000

Direct Labour Cost Rs. 5,000 and

Factory overhead is Rs. 1,500

Absorption rate of factory overhead over prime cost

Departmental Factory overhead /Departmental Prime cost * 1000

1500/15000 *100 = 10%

(Prime Cost Direct Material + Direct Labour

Suppose Rs. 2,000 are incurred on Direct Material and Rs. 800 are incurred on direct labour then the factory overhead will be charged on the basis of prime cost 2800* 10/ 100 =rupes 280

Suitability :

(a) When a standard article is produced.

(b) The article being produced requires a constant quantity of material and number of labour hours, i.e., ratio of material cost to wages must be constant from job to job and product to product. Such a situation rarely occurs, so the use of the prime cost percentage rate usually results in an inequitable allotment of overheads, i.e., it leads to under/over recovery.

Advantages :

(1) This method is very easy to compute and apply.

(2) The main argument in its favour is that both material and labour are taken into consideration while computing the overhead rate.

Disadvantages :

(l) It combines the shortcomings of both direct material and direct labour methods.

(2) Additional costs which arise due to the use of costlier machines are ignored.

(3) This method is likely to result in an inequitable allotment of overheads.

(4) There is no direct relationship between manufacturing overheads and the prime cost ofthejob concerned.

(5) Material prices frequently and widely fluctuate, so if the factory overheads are absorbed on the basis of material cost or prime cost, they would also fluCtuate violently from job to job and from period to period.

(4) DIRECT HOUR RATE OR PRODUCTION HOUR METHOD

Under this method, labour hours are taken as a basis for overhead absorption. In this method, total hours worked by labour in a department are calculated for a specified period, and the overheads of that department for that period are divided by the number of hours to get the hourly rate of overheads. The overheads pertaining to a job or product are ascertained by multiplying the number of labour hours devoted to the job or product by the hourly overhead rate. The formula for computing the direct labour hour rate for a period is :

Direct Labour Hour Rate = Facto overheads / Direct labour hours during a given period

Example : Total overhead of a year of production department is Rs. 1,800. The direct labour hours of that year are 6,000, the per hour labour absorption rate will be :

Rs. 1,800 / 6000 hours = Re. 0.30

If 200 hours are spent to complete a work, the factory overhead will be equal to 200 hours x 0.30 Rs. 60.

Suitability of Method : This method can be employed :

(1) Where most of theworkis completed manually.

(2) Where direct labour rate can be calculated for each category of workers.

(3) Upon a machine having a low operating cost in relation to the cost of labour hour.

Advantages : This method is an improvement over the percentage.on direct wages method and gives due recognition to the time factor. This method is logical one as it takes into account time factor completely. This method also appropriately charges overhead on the basis of number of hours spent in performing a particular job. Disadvantages : The disadvantages are :

(i) Like the direct labour cost method, this method does not take into account factors of production other than labour. This, method sometimes leads to faulty distribution of overhead to product cost. In a machine shop, for instance, where different types of machines are in use, it will not be correct to recover departmental overhead, on the basis of labour hours. Similarly, recovery of material handling and upkeep expenses on the basis of production labour hours will not be appropriate and for such expenses a separate overhead rate may be calculated.

(ii) Many concerns do not maintain any record of time taken on job cards. This is particularly so where wage payments are not related to either the attendance or the time taken for production, as for example in the piece-work system more clerical effort is, therefore, required in determining the overhead rate because labour time has to be specially recorded to meet the requirements of this method.

(5) THE MACHINE HOUR RATE METHOD

This method is used in those cases, where the processes of manufacture are carried out by machines and there is very little or practically no manual labour. It is determined by dividing the overhead cost to be apportioned or absorbed by the number of machine hours worked or to be worked. This can be computed by the following formula :

Overhead Rate = Factory overhead/ Machine hours during the period

Machine hour rate has been defined by lCMA, England as, “it is an actual or predetermined rate of cost apportionment or overhead absorption, which is calculated by dividing the cost to be apportioned or absorbed by the number of hours for which a machine or machines are operated or expected to be operated.” Thus, this method estimates the cost of running a machine for one hour and a job is debited with an amount of overheads, equal to the number of hours for which the machine was used on that job, multiplied by the hourly rate.

(6) COMBINED MACHINE HOURAND DIRECT

It is a combined use of machine hour and labour hour rate. In the modern time, it is found that machines and labourers, work t0 gether in the factories. So, this mixed or combined use of these methods is very fruitful. The overheads related to the machines are absorbed on the machine hour rate basis and the overheads related to labour are apportioned on the basis of labour hours.

Advantages :

(l) Production work is done by both labour and machine, therefore, this method is quite good.

(2) This method removes the demerits of machine hour rate and labour hour rate and include the advantages of both rates.

Disadvantages : This method is theoretically easy but practically very difficult to apply since it is very difficult to find out the absorption rates after dividing departmental overheads into two parts.

(7) OUTPUT BASIS METHOD

Under this method, rate of overhead absorption is calculated by dividing the overheads to be absorbed by the number of units produced or expected to be produced. The formula for computing the overhead rate per unit is given below :

Overhead rate per unit = Factory overhead / No. of units produced

For Example : The factory overhead is Rs. 8,000 and total number of units produced 40,000 then the overhead rate by using output basic will be rupes 8000/40000 = rupees 0.20. suppose 500 unit are produce then 500* 0.20 rupes 100 will be charged

Suitability :

(1) This method is suitable where production is done in the single type of units.

(2) The unit of production should be standard, e.g., gallon, litre, pound and ton, etc.

(3) Labourers do different types of sub-work at a time.

Disadvantages : It is very simple method but this cannot be used where different types of products are manufactured.

click here for next page

Follow me at social plate Form |

|||

Thnku ,it’s really helpful 😊